Table of Contents

The deferred gift annuity is a very appropriate option for donors ages 25 to 60. Like charitable gift annuity, it pays an income stream, but it also begins at a point in the future. It is a very straight forward process just like this: you make a gift, charity agrees to pay you and your second beneficiary and a stream of income for life, will beginning at a point in the future. A longer delay between the creation of the deferred gift annuity and the commencement of payments result in a higher annuity rate and a larger income tax charitable deduction.

Upon your death, the charity has the use of the remainder of your gift. You need to know that your income stream must be deferred for at least one year after gift is made. Many donors choose age 65 or older to receive the income stream because they will have retired and expect to be in a lower tax bracket. Used this way, the deferred gift annuity is similar to an IRA. Unlike the charitable gift annuity, the deferred gift annuity pays the highest rate to the youngest donors since there is a longer period of time between the date of the gift and the drawing of income. The charity invests your money for years, anticipating the time when income payments must be made.

Older donors also may use a deferred gift annuity and defer income for several years. This may be especially useful for a donor who wants to defer receiving income until some time after age 70 or later.

Benefits of deferred gift annuities include:

- Immediate charitable income tax deduction.

- Guaranteed income in the future, often at retirement.

- Excellent yield.

- Eligibility for current income tax deduction.

- Partially tax-free income.

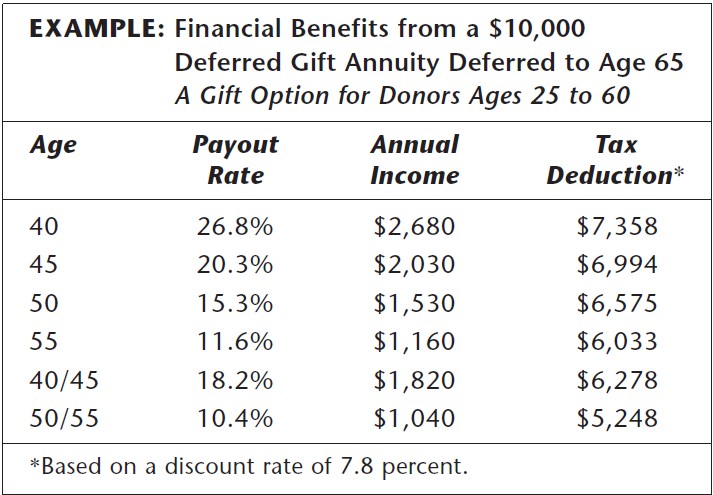

The following example presents the financial benefits from a $10,000

Image Example:

|

| deferred gift annuity deferred to age 65. |

- [message]

- Two-Beneficiary Charitable Gift Anuity Agreement Example

- Charity, a charitable corporation located in <CITY, STATE>, agrees to pay to <DONOR>, of <CITY, STATE> (hereinafter called the “Donor”), for the Donor’s life and thereafter to the Donor’s spouse, <SPOUSE’S NAME>,for (HIS/HER) life if (HE/SHE) survives the Donor, an annuity in the annual sum of <AMOUNT IN WORDS>, (<DOLLAR AMOUNT>) from the date here of, in equal quarterly installments of <$> on the last day of March,June, September, and December; provided, however, that the Donor may by the Donor’s last will revoke the annuity to be paid to the Donor’s said spouse. The first installment shall be payable on <DATE>. This annuity shall be nonassignable, except in the case of a voluntary transfer of part or all of such annuity to Charity. The obligation of Charity to make annuity payments shall terminate with the payment preceding the death of the survivor of the Donor and the Donor’s said spouse, unless the Donor revokes the annuity payable to the Donor’s said spouse, in which case <ORGANIZATION’S> obligation shall terminate with the payment preceding the death of the Donor. Charity certifies that the Donor, as an evidence of the Donor’s desire to support the work of Charity and to make a charitable gift, has this day contributed to Charity $ _______, receipt of which is acknowledged for its general charitable purposes. The annuity agreement has been entered into in (State of Charity’s primary office) and is governed by the law of the <STATE> (Charity’s Primary office). IN WITNESS WHEREOF, Charity has executed this instrument this day of , 20 . For Charity:____________________ By:_______________________ <NAME>, <TITLE>

Charitable Income Tax Deduction:

The charitable income tax deduction is used in the year the gift is made, not in the year you begin receiving the income. The charitable income tax deduction is typically quite high, averaging about 50 to 70 percent of the gift. The charity will calculate the charitable income tax deduction for you. For example, a 55-year-old donor who makes a $10,000 deferred gift annuity to a charity and begins receiving payments at age 65 obtains approximately $6,033 as a charitable income tax deduction. The charitable income tax deduction is based on your age, current discount rate, and frequency and timing of payments. More frequent payments will reduce your charitable income tax deduction, as will receiving a payment at the beginning of the payment period rather than at the end of the payment

period.

I am a crypto hobbyist, i offer Tips and Reviews on the best blockchain technology, crypto assets, emerging fintech trends, Country flags, banks virtual accounts, and the best Paying Legit Networks.

Check out my Latest Articles in the Following Categories here:

Cryptocurrency Payment System Countries Credit Card Reviews